|

|

|

What Canadians Received

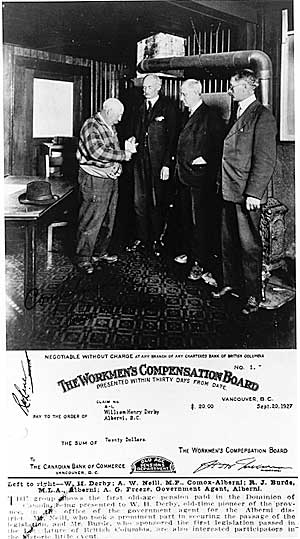

Pensions for the aged poor had been debated in Canadian politics since the early years of the century, but it was not until 1927 that the first meaningful step was taken in that direction. After the First World War, pensions were paid to soldiers who were disabled in the European conflict and to the survivors of those killed. As well, private pension plans for Canadian workers received a boost when the federal government passed legislation in 1919 permitting tax exemptions for employee contributions. In 1924, a new Superannuation Act was passed for federal civil servants, improving on earlier arrangements and providing allowances for widows and children of deceased employees. On July 1, 1924 a Special Committee of the House of Commons, appointed by the federal government, recommended a non-contributory scheme of $20 per month. This would be paid to those aged 70 or older, with costs to be shared equally between the provinces and the federal government. After considering the views of provincial governments and in particular constitutional aspects of the problem, these recommendations were embodied in a resolution placed before the House on March 26, 1926 by the Acting Minister of Labour. Following passage of this resolution, the House considered and passed an Old Age Pensions Bill on May 28, 1926. The Senate, however, rejected the bill. The Senators were themselves entitled to retirement benefits of $4,000 per year which, adjusted for inflation, would be worth the equivalent of $41,247.71 in the year 2000. (In all instances, Bank of Canada Inflation Calculator www.bankofcanada.ca/en/rates/inflation_calc.html was used to calculate amounts in 2000 dollars.) An identical resolution and bill were presented to the House and passed a year later on March 4, 1927. On this second occasion, the Senate quickly passed the bill, and it was given royal assent on March 31, 1927. With the passing of the Old Age Pensions Act in 1927, which established a national non-contributory, means-tested pension, the neediest seniors were finally given serious attention. Under the new Old Age Pensions Act, a maximum of $20 per month or $240 per year was paid to people 70 years of age and over whose total yearly income, with the pension benefits, did not exceed $365. An applicant whose spouse did not receive a pension in his or her own right was permitted a total income of $490 per year. Two-pension couples could have an income of $730. The maximum Old Age Pension benefit of $240 per year would have a purchasing power equivalent to just over $2,500 in the year 2000, when adjusted for inflation. Today's Old Age Security payments are about twice that amount. Eligibility was restricted to British subjects who had lived in Canada for 20 years, and to people who had been naturalized for at least 15 years and had resided in Canada for 25 years. All must have lived in the paying province for five years prior to the receipt of benefits. In addition, applicants were not permitted to transfer their property to someone else in order to fall below the income threshold. Pensioners who moved abroad lost their benefits for as long as they remained outside of Canada. Notably, the Old Age Pension did not involve a loss of voting rights, as had been the case with earlier public poor relief. Because social welfare matters fell within provincial jurisdiction under the British North America Act, the provinces were to pay the pensions, but a cost-sharing arrangement was worked out in which the federal government would issue conditional grants to reimburse them for 50 per cent of their benefit costs. This was the first federal-provincial cost-shared social program. There would be more of these cost-sharing arrangements in the future. The federal government would determine eligibility requirements and set maximum benefit figures. The provinces tailored the plan's implementation to suit their individual circumstances, and paid for its administration. Before joining the Old Age Pension program, provincial governments would pass their own legislation allowing them to sign an agreement with the federal government for that purpose. While the $20 per month stated in the Old Age Pensions legislation was a maximum, the provinces had discretion to decide what an individual's needs actually were. Eligibility for the new pension was sometimes very stringent and benefits often fell below that amount, especially in provinces where money was tight.

When administering the means test for the Old Age Pension, provincial officials looked at all possible sources of income, including property and assets or relatives who might provide assistance. If these sources were judged to provide more than $125 per year, the pension would be reduced so that the total income, including benefits, remained within the allowable figure of $365 per year, or $1 per day. It is not entirely clear from where the figure of $365 per year, or $1 per day, was derived, but the House of Commons Special Committee studying the question of old age pensions in 1924 was very attentive to levels of relief provided in municipalities across Canada. Although there was great variation, a number of municipalities were paying $1 per day in relief to their senior residents. This was only a fraction of the average worker's wage at the time. The committee also looked at the experience of other industrialized countries, and the example of Australia attracted attention. That country was paying an old age pension of about $19 per month. In the debates over old age pensions, the cost to the federal government was a dominant concern. In a lively debate over the Old Age Pensions Bill in the House of Commons on March 3, 1927, the issue of generous pension benefits for public servants was raised. One Member of Parliament noted that judges received as much as $5,000 to $6,000 per year in pensions (between $52,523 and $63,028 in year 2000 dollars). They were not begrudged these benefits; there was no argument that they should have put sufficient money aside to provide for themselves after retirement. However, working people were being expected to do what public officials were not - look after their own old age - and on far less income. At the start of the new program, the federal government's role was carried out by the Department of Labour, the same body that had been administering the Government Annuities scheme since 1922. There was also continuity with the past in an agreement between the federal government and the provinces that, in some cases, provincial officials could act to recover all benefits, plus five per cent annual interest, from the estates of deceased Old Age Pension recipients. The idea that a pension ought to be paid back is an apt demonstration of the distance yet to be covered to reach our present-day conception of public pensions as a right earned through the obligations and privileges of citizenship. However, the recovery of benefits from estates were reflective of cost concerns, and when they were made, the Canadian government would be reimbursed for its share of the pension payments. Canada's first old age pension scheme was intended to help only the most desperate seniors. It excluded status Indians because of their separate treatment under the Indian Act, but it was an improvement on earlier poor relief methods. In spite of an intrusive "means test" and the threat to an applicant's property implied by the right of officials to reclaim costs from estates, the fact that seniors could receive public financial assistance on a regular guaranteed basis, even if they had an income, was an important precedent. |

||||||||||||||||||||||||||||